You keep hearing on news channels that Pakistan has signed another IMF loan Pakistan agreement. What does that mean for a common citizen? Simply put the International Monetary Fund lends money to countries like Pakistan when they run out of currency to pay for imports like oil, machinery, or medicine. In return, the IMF asks the country to fix its economic problems. This article explains the IMF Loan program in simple words. By the end, you will understand why the IMF gets involved in what conditions come with the loan and how it affects your grocery bill, electricity tariff, and job prospects. Let us break down the IMF Loan package step by step. Finally, we will see how this loan connects to broader Pakistan Economic Reforms.

What is an IMF Loan?

The IMF is like a credit union for countries. When a member country faces a balance of payments crisis – meaning it cannot pay for imports or repay old debts – it approaches the IMF for emergency financing. In Pakistan’s case the IMF Loan programs have been recurring since the 1980s. The recent one, approved in 2025, is a $7 billion (about $22 per person in the US) Extended Fund Facility over 37 months (about 3 years).

Why Does Pakistan Keep Going to the IMF?

Pakistan’s economy has a big problem: it imports more than it exports. To fill the gap, it borrows money. Over time, debt repayments have become larger than loans. The government also spends a lot on subsidies, loss-making state enterprises and defense leaving little for development. When foreign reserves fall below three months of imports the IMF steps in. The IMF Loan programs aim to provide a bridge while Pakistan implements tough economic reforms to reduce its dependency on foreign loans.

How the IMF Loan Program Works

Here is how it works in four steps:

- Step 1: Request and Negotiation: The Pakistani government sends a letter of intent to the IMF acknowledging problems and promising corrective actions. Then months of negotiations happen.

- Step 2: Board Approval: Once a staff-level agreement is reached, the IMF’s Executive Board votes. After approval, the first tranche is released.

- Step 3: Quarterly Reviews: The IMF does not give all the money. Every three months it checks if Pakistan has met performance targets. If Pakistan fails a review the next tranche is delayed.

- Step 4: Completion and Repayment: After all reviews are passed, the full loan is disbursed. Pakistan then repays the IMF over years with interest.

Simple Table: IMF Loan Programs, for Pakistan

| Program Year | Facility Type | Loan Amount | Duration | Status |

| 2013-2016

2019-2022

2023

2025-2028 |

EFF

EFF

Stand-By Arrangement

Eff |

$6.6 billion (about $20 per person in the US)

$6 billion (about $18 per person in the US)

$3 billion (about $9.2 per person in the US) Eff |

36 months 9 months (about 3 years)

39 months (about 3 and a half years)

9 months

37 months (about 3 years)

|

Completed

Derailed early

Completed

Active

|

Key Conditions Attached to the IMF Loan to Pakistan

This is an important part for citizens. The IMF Loan Pakistan does not come free. Each condition directly changes life.

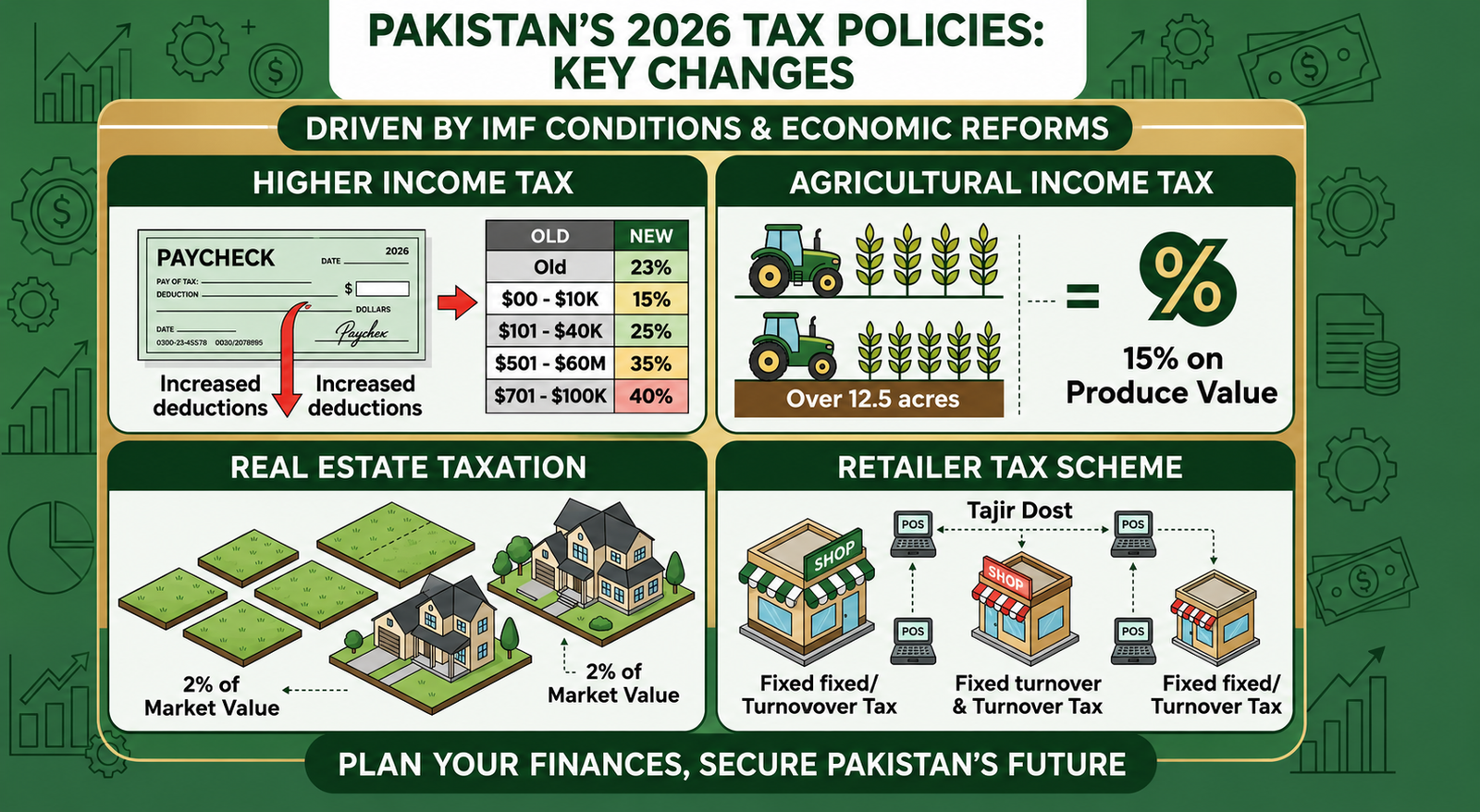

Condition 1: Fiscal Consolidation (Higher Taxes)

The IMF demands that Pakistan raises its tax-to-GDP ratio from below 10% to over 13% by 2028. How? By bringing retailers, estate, and agriculture into the tax net. For people this means:

- Higher general sales tax on -essential items.

- Removal of tax exemptions on goods, such as packaged food and mobile phones.

- New property taxes based on market value.

Condition 2: Energy Subsidy Reform

Electricity and gas subsidies cost Pakistan over PKR 2.5 trillion in 2024. The IMF wants those subsidies eliminated except for the 15% of households. As a result:

- Households using than 300 units per month will see tariff hikes every quarter.

- Industrial tariffs will be linked to fuel prices.

- Cross subsidies, where commercial users pay for users, will be phased out.

Text Graph: How IMF Conditions Reduce Subsidy Burden (Projected)

Year Total Energy Subsidy (PKR billion) % of GDP

- 2025 3200 4.2%

- 2026 2400 3.0%

- 2027 1600 1.8%

- 2028 900 0.9%

Condition 3: Exchange Rate Flexibility

The IMF insists that the State Bank of Pakistan stop pegging the rupee artificially. Instead, the rupee should find its level based on demand and supply. This has already led to two devaluations in 2025-2026. A weaker rupee makes imports expensive such as petrol, cooking oil, and medicine. Helps exporters.

Condition 4: Tight Monetary Policy

To control inflation, the IMF wants interest rates with a policy rate above 18% for most 2025-2026. This makes loans for cars, houses, and businesses expensive. Savings accounts earn more. Borrowing becomes painful.

Condition 5: SOE Privatization

Pakistan must sell loss-making state-owned enterprises, such as PIA, Pakistan Steel, and power distribution companies. The IMF sees privatization to stop bailouts. For workers, this may mean layoffs.

How the IMF Loan Affects an Ordinary Pakistani Family

Let us take a middle-class family in Lahore with two children, a salaried father and a mother who runs an online boutique. Under the IMF Loan Pakistan program here is what changes:

- Monthly grocery bills increase 12-15% due to GST and import costs.

- Electricity bill for 400 units jumps from PKR 10,000 to PKR 13,500.

- Car loan EMI for a 1.3L car goes up by PKR 8,000 due to interest rates.

- Mother’s boutique faces raw material costs, such as imported fabrics but also gets cheaper export financing if she starts selling abroad.

- Father’s salary might not rise fast as inflation but if the reforms succeed job security improves after 2-3 years.

Observations from Implementation (2025-2026)

Based on data from the first three quarterly reviews of the current Pakistan Economic Reforms here are real-world observations:

Positive Observations:

- Foreign reserves have increased from 8 billion to 12.5 billion, reducing fear of default.

- Remittances rose 14% in six months because banks offer exchange rates.

- The stock market rallied 35% since the program started indicating investor confidence.

Negative Observations:

- Inflation remains above 19%, squeezing middle classes.

- Small businesses are closing due to electricity costs and tax compliance burdens.

- Political instability increased, with opposition parties holding street protests IMF conditions.

Neutral Observation:

- The government has successfully expanded the Benazir Income Support Programmer to cover 9.5 million families, offsetting subsidy cuts. However, many deserving families are still not registered.

Analysis: Pros and Cons of IMF Loan for Pakistan’s Economy

- Foreign Reserves prevent default on imports and debt payments comes with strict monitoring.

- Inflation brings it down gradually (from 30% to 19%) short-term pain with utility bills.

- Investment attracts FDI and World Bank co-financing IMF conditions scare some local businesses.

- Government Spending forces reduction in wasteful subsidies cuts in development budget (less new roads/schools)

- Exchange Rate unified market rate ends currency smuggling rupee devaluation raises all import prices.

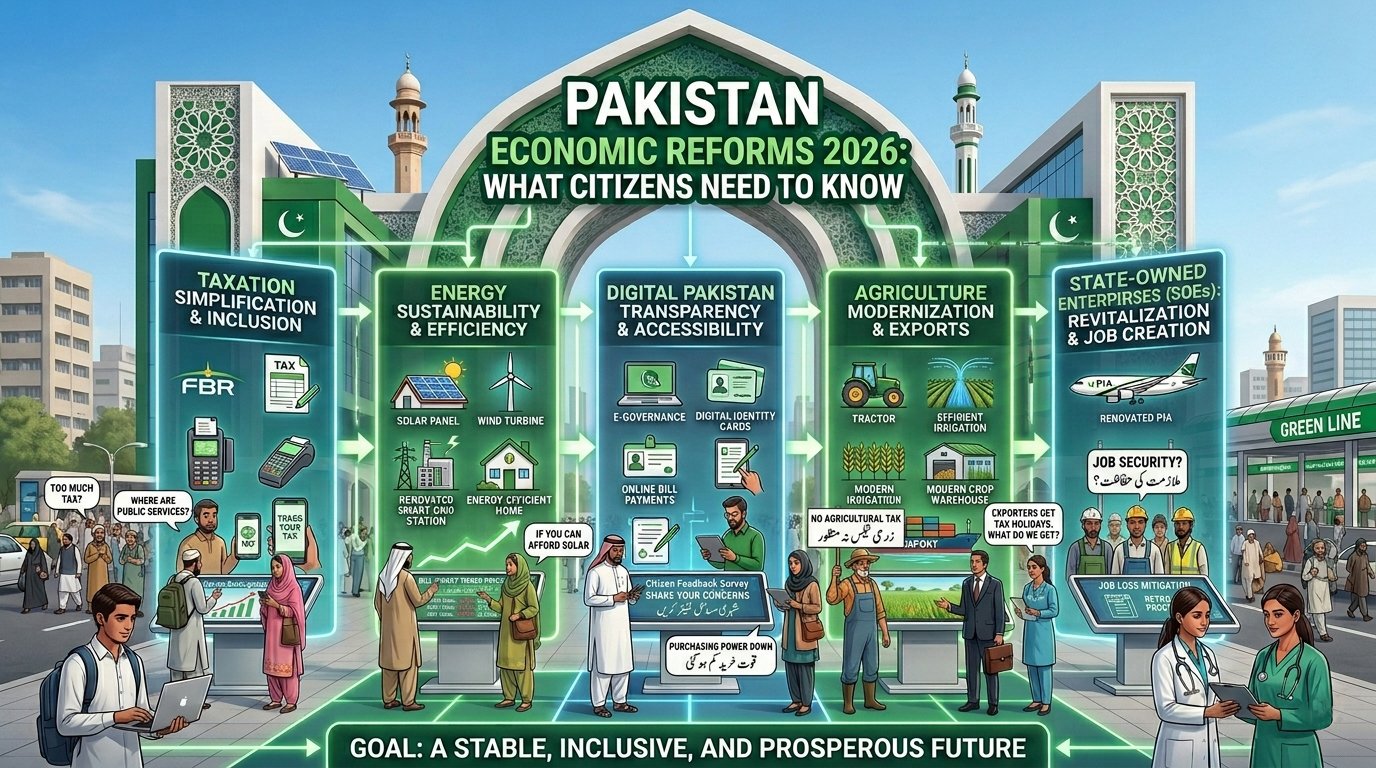

Connection to Pakistan Economic Reforms

You will see that the IMF Loan Pakistan is not a one-time thing. It is always connected to a lot of changes. This is where Pakistan Economic Reforms come in. The 2026 reforms include making the FBR digital automating GST refunds having a sales tax and creating a sovereign wealth fund for SOEs. Without these Reforms, the IMF will not give Pakistan the loan money. In words: the loan is like a reward, and reforms are like a warning. The government has said that many of these reforms should have been made a long time ago. It is only when the IMF puts pressure on them that Pakistani governments make tough decisions. For citizens, this is a situation. You suffer now but if reforms work, the economy will be stronger.

Pakistan deficit

Let us talk about one big problem that the IMF always looks at: the Pakistan fiscal deficit. This is the difference between what the government earns and what it spends. In 2025 the fiscal deficit was 7.6% of GDP. Which is extremely high. The IMF program wants to reduce it to 3.8% by 2028. How will they do this? By collecting taxes and cutting unnecessary spending. If Pakistan can do this it will not need to borrow a lot of money from banks, which will help the sector. So, it is clear: the IMF loan is a way to reduce the Pakistan deficit, and a smaller deficit means lower prices and lower interest rates overall.

A Difficult but Necessary Step

The IMF Loan Pakistan program is not a gift. It is a lifeline with rules. For citizens, the next two years will be tough. Higher bills, more taxes, and fewer subsidies. But the alternative would be much worse: no fuel, no medicine, closed factories, and high prices. By understanding why Pakistan needs the loan you can plan your budget better avoid debt and even find opportunities in areas like exports or IT that benefit from an exchange rate.

The main point is this: The IMF Loan Pakistan is making Pakistans leaders do things they have been avoiding for a time. If citizens can manage the short-term difficulties and make sure the government is transparent Pakistan can finally stop relying on bailouts every year. That is hope, behind all the economic talk.